100k Tax Trap

💸 The £100k Tax Trap: What High Earners Need to Know

If you’re earning around £100,000 or more, your payslip might not tell the whole story. Due to a hidden rule in the UK tax system, you could be paying an effective marginal tax rate of 60% or higher — without realising it. This page explains why it happens, who it affects, and what you can do to keep more of what you earn.

🤔 What’s the £100k Tax Trap?

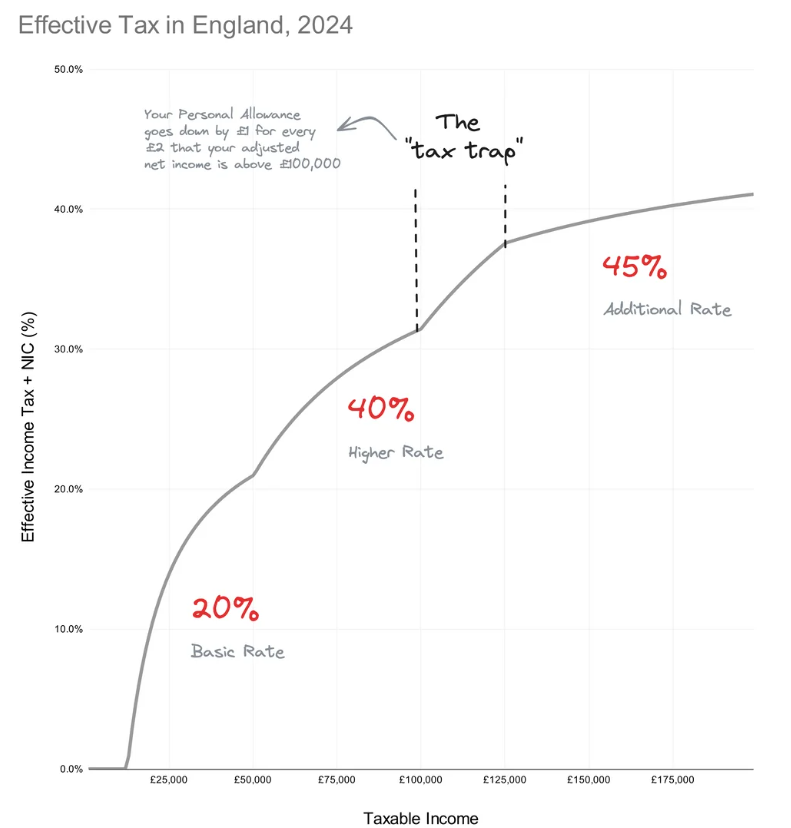

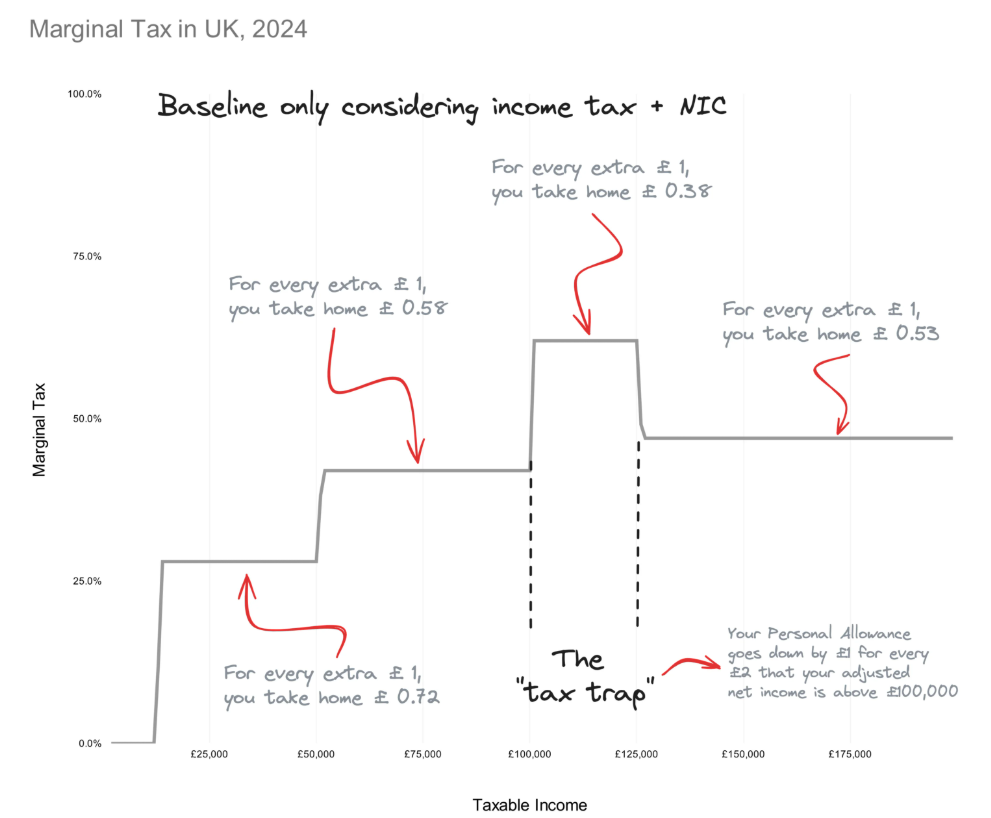

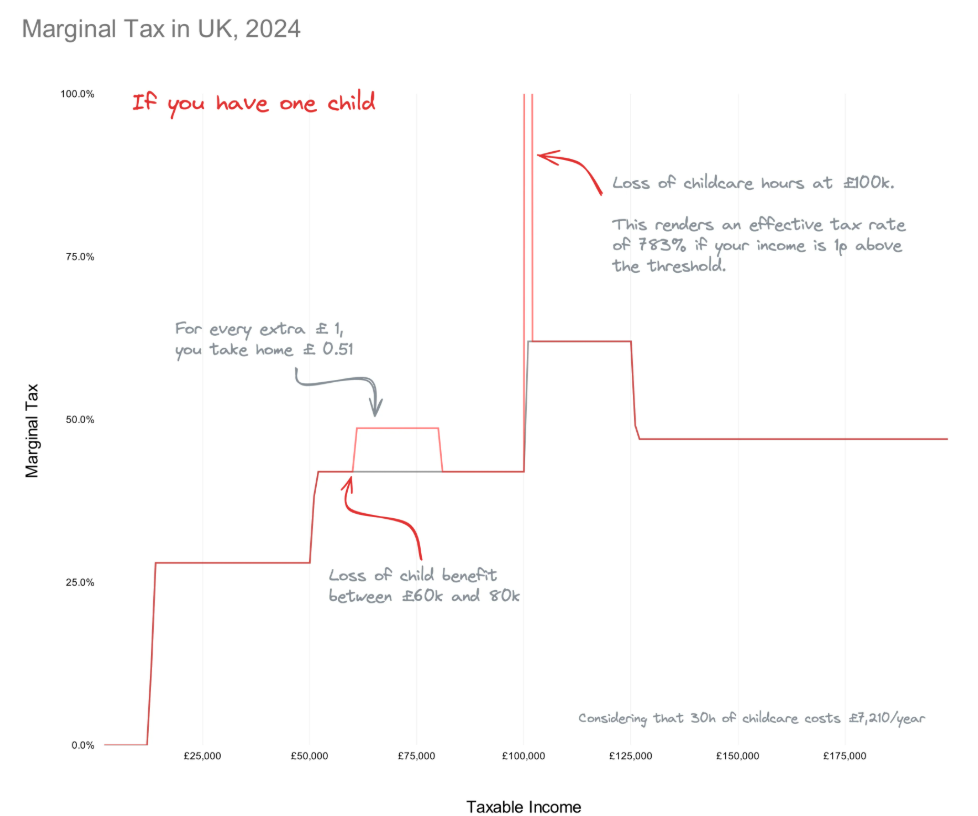

The £100k tax trap kicks in when your adjusted net income crosses £100,000. From that point, your Personal Allowance (£12,570) is gradually removed — £1 for every £2 you earn above the threshold.

The tapering works like this: for every £2 you earn over £100k, £1 of your Personal Allowance is removed. That creates an effective 60% marginal tax rate across that band — because:

- You pay 40% on the income itself

- And another 40% on the previously tax-free amount now being taxed

Example: At £110,000 income, you lose £5,000 of allowance — that’s £2,000 in extra tax on top of the £4,000 due on the £10k income above £100k.

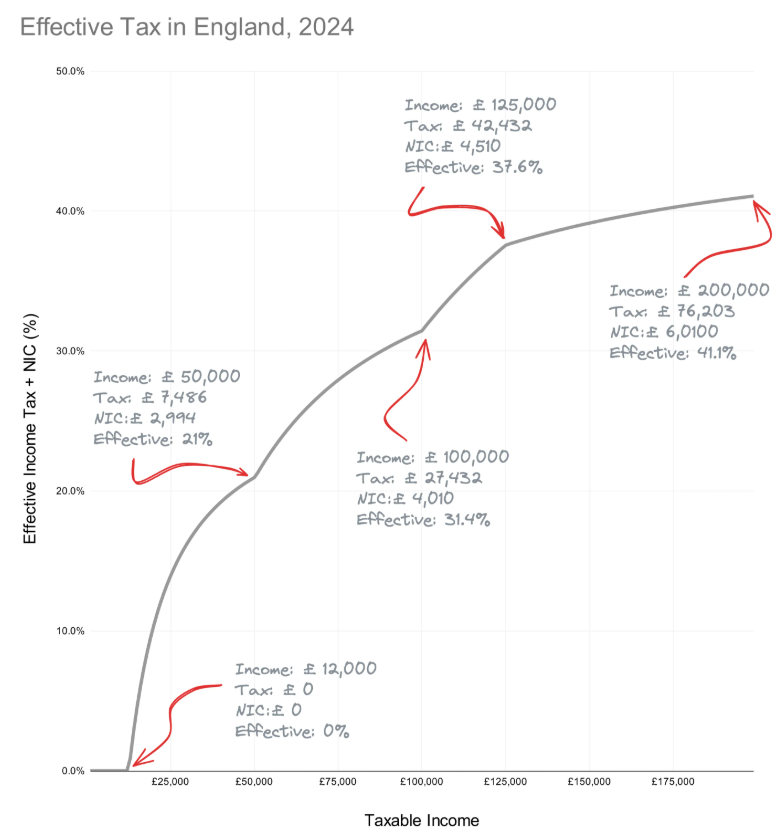

📉 Real Example: Effective Rate Breakdown

| Income | Allowance Lost | Tax Due | Effective Rate |

|---|---|---|---|

| £101,000 | £500 | £600 | 60% |

| £110,000 | £5,000 | £6,000 | 60% |

| £120,000 | £10,000 | £12,000 | 60% |

Source: HENRYUK Calculations

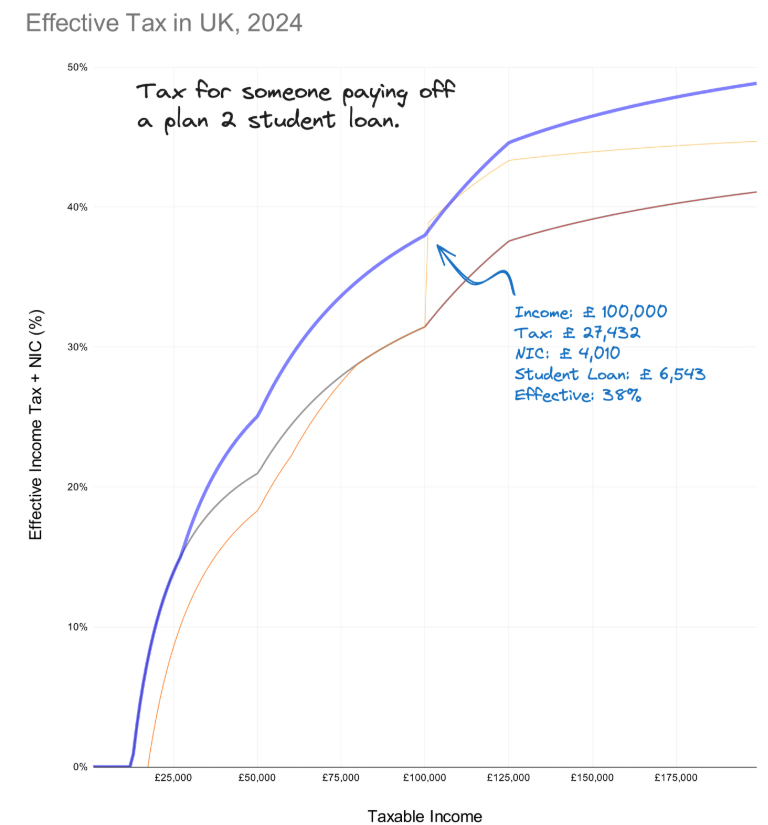

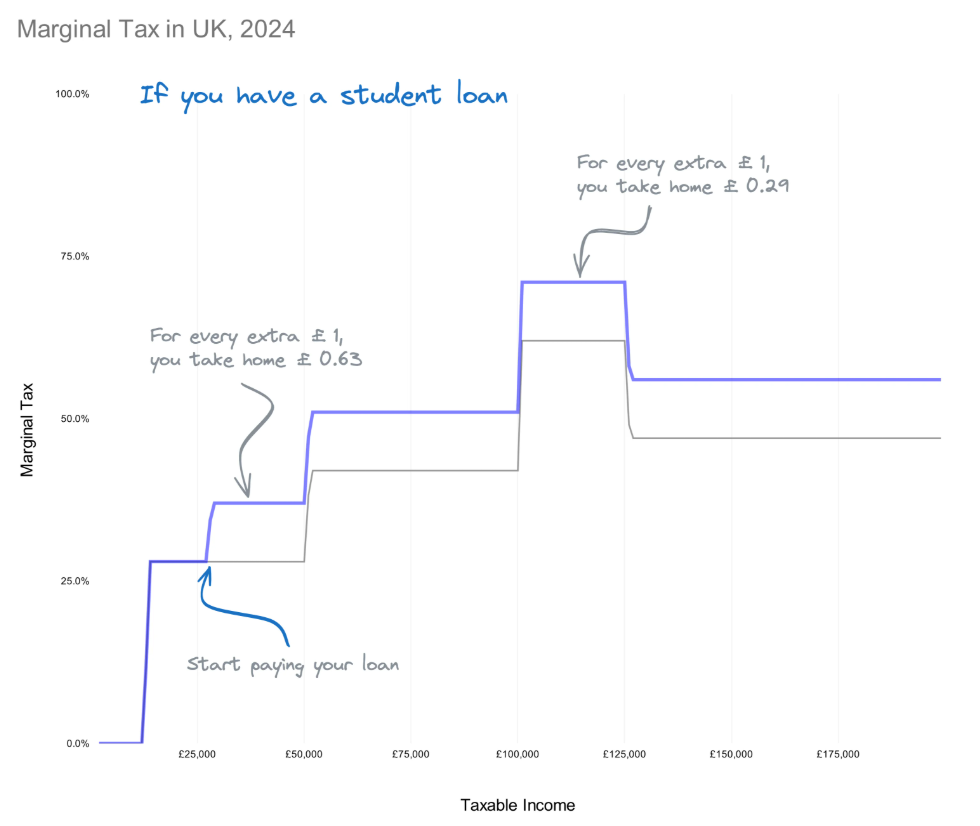

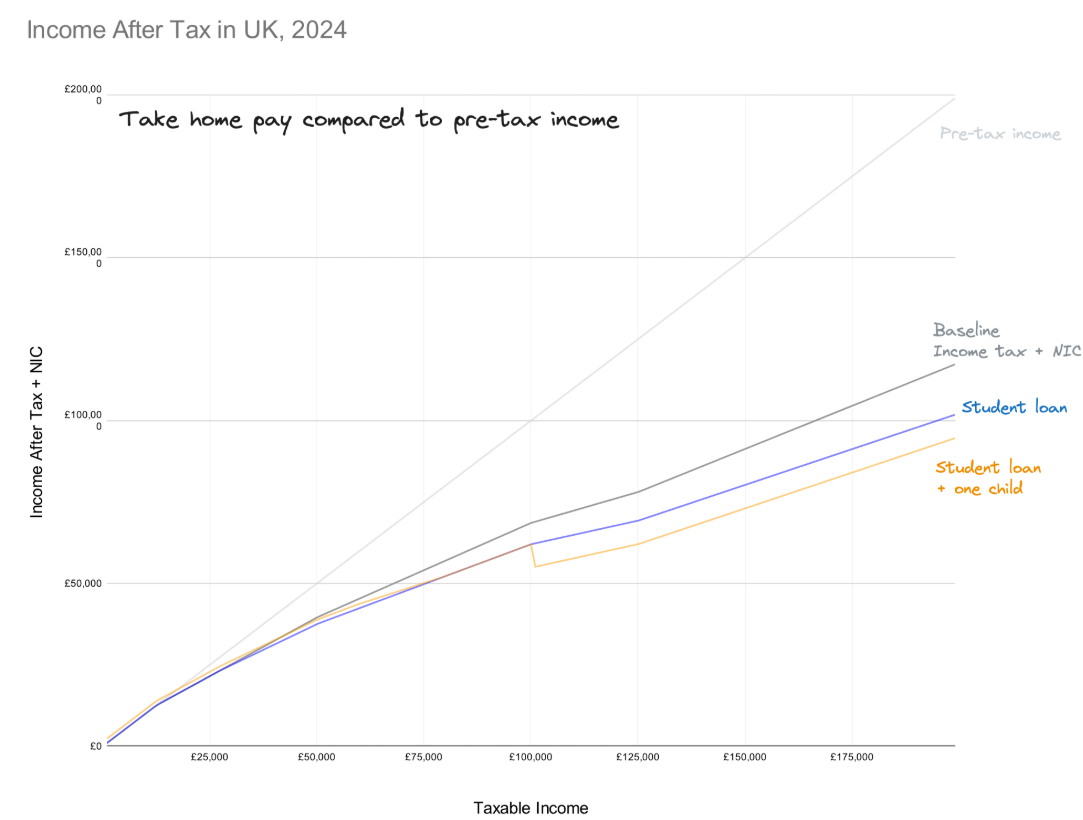

📌 Don’t forget National Insurance (NI): You also pay 2% NI on income above £50,270. That pushes your marginal rate from 60% to 62% on earnings in the £100k–£125,140 range. If you also repay a student loan, it could reach as high as 71%.

🧮 Adjusted Net Income: What Counts?

This is the number HMRC uses to decide if you lose your personal allowance. It includes:

- Salary, bonuses, rental income, dividends, savings interest

- Minus: Gross pension contributions, Gift Aid donations, salary sacrifice deductions

🔧 How to Avoid or Reduce the Tax Trap

1. Pension Contributions

Putting money into a pension is one of the most efficient ways to reduce adjusted net income.

Note: If your total contributions approach or exceed the annual limit (£60,000 for 2024/25), you may still be able to contribute more using carry-forward. This lets you use unused pension allowances from the last three tax years — as long as you were eligible and contributed to a registered scheme during those years.

- Salary sacrifice: Done before tax, lowers income and National Insurance

- SIPP or personal pension: Contribute post-tax, then claim back relief via Self Assessment

2. Gift Aid Donations

Charitable giving can also reduce adjusted net income — and earn you tax relief at your marginal rate.

- Donating £4,000 with Gift Aid = £5,000 gross

- You reclaim the higher-rate difference (20%) via Self Assessment

- You can even backdate donations to the previous tax year if declared early

3. Bonus Timing or Deferral

If you’re expecting a bonus around March, ask your employer if it can be deferred to April. That pushes it into the next tax year and could keep your current year income under £100k.

4. Other Adjustments

- Cycle to Work: No BiK, lowers gross income

- Buying holiday days: Works like salary sacrifice, no BiK

- Payroll Giving: Pre-tax donations reduce taxable income (no NI relief)

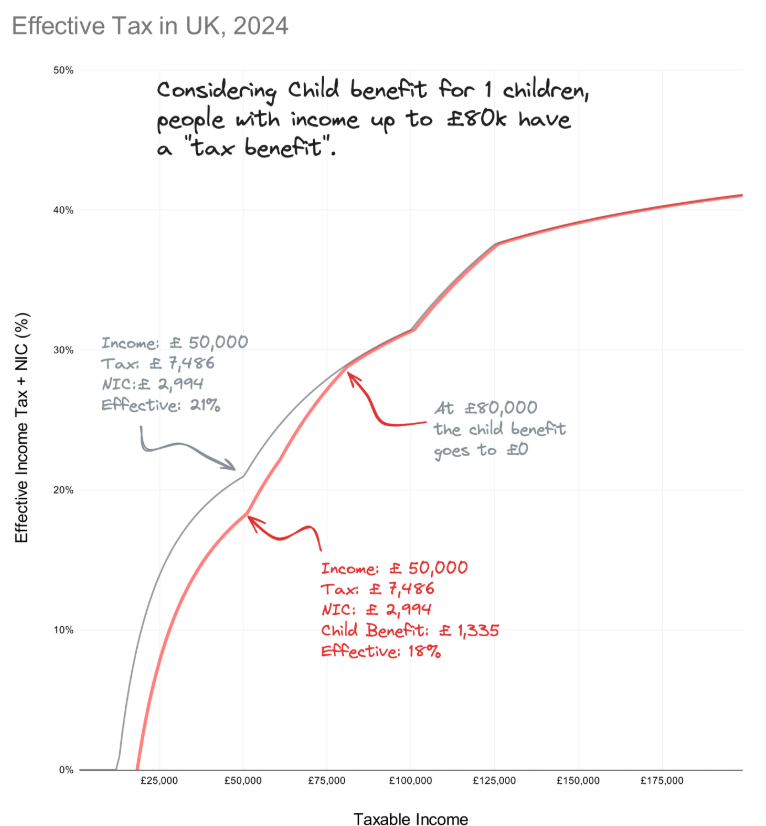

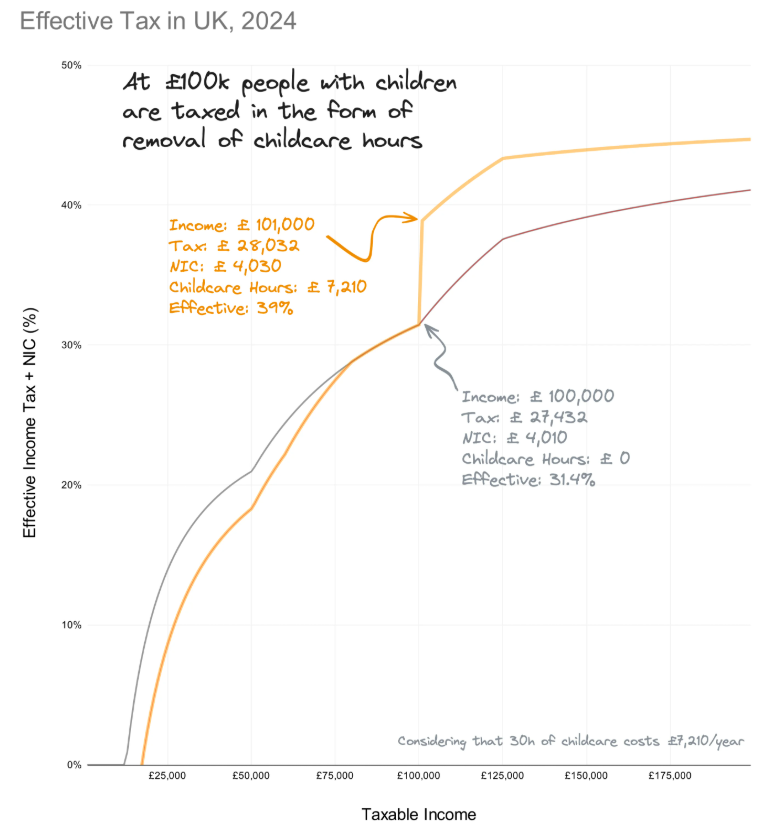

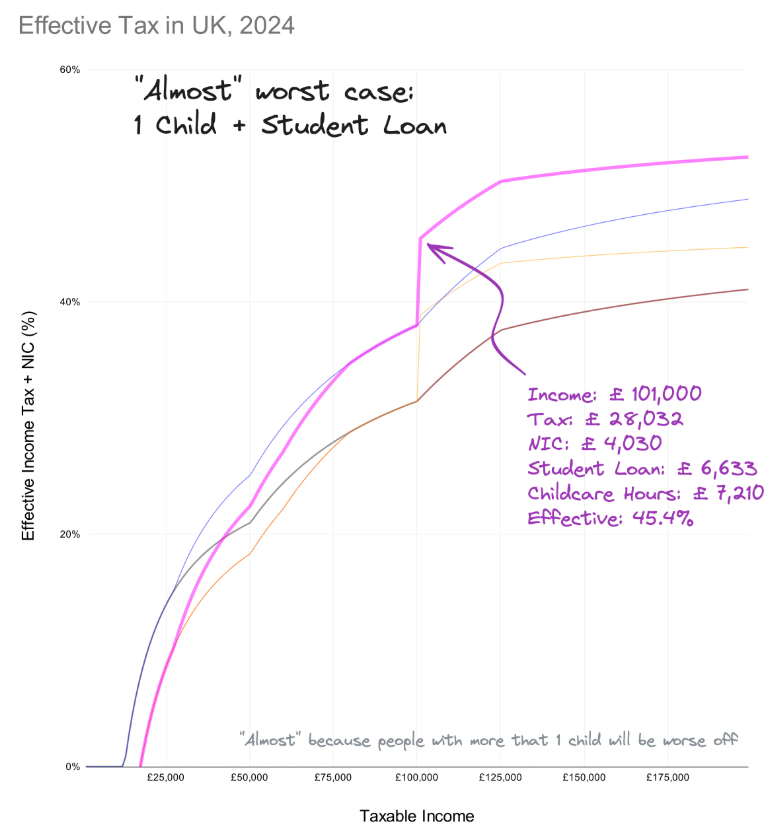

👶 The Family Penalty

Reaching £100k doesn’t just mean higher tax — it also removes access to benefits like:

- Tax-Free Childcare (worth up to £2,000 per child)

- 30 free childcare hours

This makes tax planning even more important for working parents.

🧾 Do I Need to File a Self Assessment?

If your adjusted net income exceeds £100k — or you’re claiming higher-rate relief on pensions or Gift Aid — you likely need to file.

⚠️ PAYE Pitfall: If your income fluctuates above/below £100k year to year, HMRC may miscalculate your tax code or adjust it mid-year. This can result in overpaying or underpaying tax — especially if you claim Gift Aid or make pension changes.

✅ Check your tax code regularly via the HMRC app or online portal. You could be due a refund.

📊 Shown Visually

The following visuals illustrate how the tax trap works, how income affects personal allowance, and how pension contributions can rescue you from the trap. Created by u/MolecularDev from r/HENRYUK.

Visuals by u/MolecularDev on r/HENRYUK

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please speak to a qualified adviser before making financial decisions.